Our approach to BCH adoption has shifted from simply offering value-added services to following a more structured, sustainable path. By focusing first on grassroots support, then scaling through practical utility and community empowerment, we can lay the groundwork for long-term growth and meaningful institutional adoption.

Over the past six months, our experience on the ground has reshaped how we think about sustainable adoption of Bitcoin Cash (BCH). When we launched our first Flipstarter campaign, our core strategy revolved around building value-added services into the wallet—services designed to attract merchants and customers to use BCH in meaningful ways.

While that approach was directionally correct, we now realize it was incomplete.

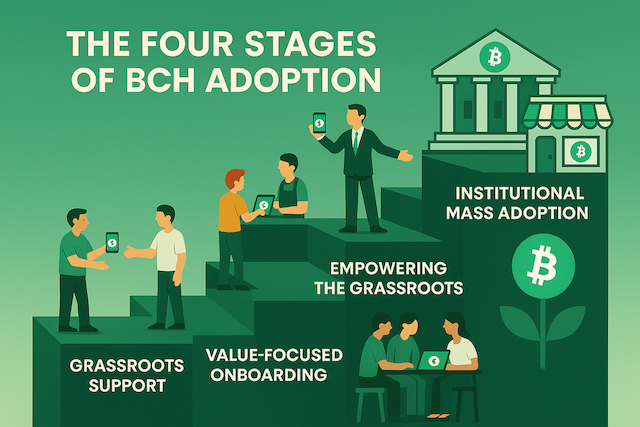

To maximize impact and avoid costly missteps, we’ve refined our adoption framework into a four-stage model , which we believe more accurately reflects the necessary progression toward sustainable, large-scale adoption.

The Four-Stage Model of BCH Adoption

Stage 1: Grassroots Support

This foundational stage is all about building a functional ecosystem from the ground up.

- Organize interest groups of crypto-savvy individuals who are already inclined to spend BCH.

- Onboard merchants who are relevant to these groups—ensuring real usage from day one.

- Gradually introduce value-added services that make BCH more useful—like bill payments, digital products, and in-app promotions.

- Maintain balance : grow both interest groups and merchant coverage in tandem. Onboarding merchants with no BCH-spending customers is wasteful and creates negative perceptions.

Stage 2: Value-Focused Onboarding

Once a core user-merchant loop is functional, the next step is to appeal to broader users through real value, not ideology.

- Lower the cost and improve the usability of value-added services, making them more attractive than fiat-based alternatives.

- Use value as the main pitch —skip the talk about blockchain or decentralization, which can alienate the average person.

- Let the product sell itself : if using BCH via Paytaca saves time or money, users will adopt it organically.

Stage 3: Growth by Empowering the Grassroots

At this stage, we shift from centralized to community-driven growth.

- Equip local group organizers with the tools, training, and strategies to launch local adoption initiatives.

- Incentivize onboarding efforts through commissions, transaction-based revenue shares, or token rewards—creating long-term motivation.

- Support builders and startups developing new applications and services that utilize BCH and integrate with Paytaca.

Stage 4: Institutional Mass Adoption

Only once a critical mass of users and merchants is established should we pursue large-scale partnerships.

- Broker partnerships with big businesses—like retail chains, remittance companies, insurance providers—who can instantly amplify reach.

- Launch large-scale marketing campaigns , leveraging both traditional and digital channels to drive awareness.

- Engage government agencies for partnerships around digitalization and financial inclusion, positioning Paytaca as a trusted non-custodial platform.

Why This Model Matters

Recognizing and respecting the natural progression of adoption ensures that our efforts are scalable, cost-effective, and impactful. Skipping stages, such as going after big institutions without grassroots support, often leads to partnerships that are hard to sustain or fail to translate to real usage.

This model isn’t static—it will continue to evolve as we gain new insights. But it gives us a roadmap grounded in what works: building real utility, empowering communities, and scaling with purpose.